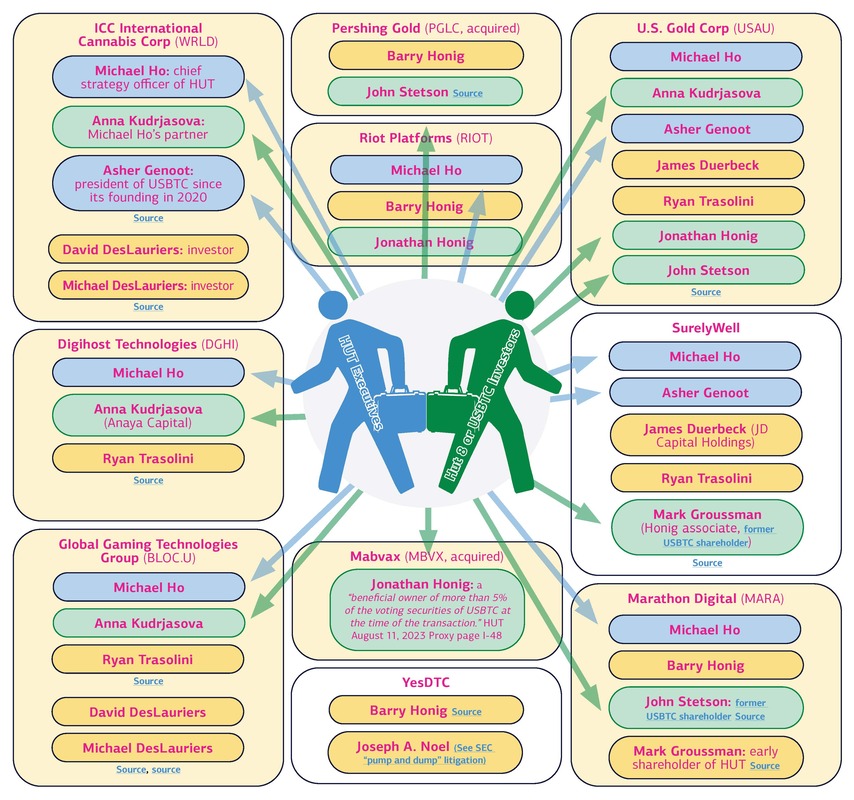

Be warned. We are activists, usually on the short side. We are biased.

We do our best to find and present facts, based on extensive primary research and using public sources.

But we will profit if these stocks decline or, when we are long, rise in value.

We do not offer advice on how to trade a stock. We present our views.

We do our best to find and present facts, based on extensive primary research and using public sources.

But we will profit if these stocks decline or, when we are long, rise in value.

We do not offer advice on how to trade a stock. We present our views.

J Capital is short AXT, Inc. (NASDAQ: AXTI)

AXTI may be on the brink of collapse:

Chinese headlines say its local IPO has failed. Its revenue is plummeting,

and creditors are at the door:

The Chinese reports AXTI doesn’t want you to see

- AXT Inc (AXTI), a manufacturer of geranium, gallium arsenide, and indium phosphide (key ingredients for LED and semiconductor chips) saw a 140% increase in share price in February, following management’s enthusiasm about AI opportunities.

- AXTI is listed in the U.S., but its business operations are almost all conducted through a subsidiary in China. AXTI wants to list that subsidiary in Shanghai to capture new financing. But the listing prospectus attracted unexpected scrutiny and unveiled a plethora of undisclosed issues in China. Our research has found those issues are only the tip of the iceberg.

- The listing vehicle raised $49 mln from private investors at a sky-high valuation in 2020. AXTI expected to capture much more investment at the time of the IPO. But it has been 18 months since the last IPO update, and U.S. investors haven’t been told that the IPO has apparently been blocked by Chinese regulators.

- In March 2023, Chinese press reports said: AXTI’s subsidiary, Tongmei, saw its “IPO blocked: The U.S. semiconductor ‘shell company’ was split off for [a local] listing, related-party transaction prices were unfair, and the authenticity of company performance was questionable.”

- We have uncovered a deluge of reasons why Chinese regulators potentially blocked this IPO, including falsifying data, tax evasion, improper storage of hazardous chemicals, suspicious related-party transactions, IP litigation, and defaulting on wages to employees.

- Sales have collapsed by over 50%, and there is no reason to believe that AXTI can revert to its formerly reported margins and sales numbers, despite the claims that they make about AI demand.

- We learned from interviews with former managers in China that production volume is down by at least 50% and sometimes up to 90%. They said production efficiency has also plummeted. Formers we spoke with see no end in sight to the low production.

- When AXTI applied for its Chinese IPO, related-party purchases and sales were over 50% of revenue. Chinese regulators have expressed deep concern about those transactions.

- AXTI’s production has been halted more than 10 times for environmental problems over the last five years. Chinese reporters depict this behavior as "puzzling" and point out that the company’s attitude toward regulation is almost one of disregard. There is no clear pathway for AXTI to fix these issues and get the Shanghai IPO, which is needed to fund further expansion.

- Among the environmental woes: a government report points to arsenic contamination in the groundwater. We also learned in interviews of a 2020 fire at the Beijing factory that has not been disclosed to U.S. investors. That and the use of hazardous chemicals forced AXTI’s factory to move half its production to facilities 300 miles away, meaning some production involves shipping materials on a 7-plus hour truck ride.

- We show that the $99.3 mln at cost in buildings reported by AXTI is very unlikely. The buildings consist principally of a ramshackle factory in Beijing and a lot of dormitories in a tiny rural county in Liaoning.

- We think AXTI’s inventories— which have soared to 1.3 years while sales fell - may not be there or may be dramatically overstated in value.

- We have also uncovered potential nefarious activities related to the IPO by AXTI’s Chinese underwriter, Haitong Securities. Two related parties of Haitong Securities invested in the AXTI IPO, potentially to drum up interest and inflate the orderbook. Not only has Haitong Securities had 16% of its IPOs withdrawn, but it has been sued numerous times and warned by the CSRC. Haitong was forced to disgorge ¥28.6 mln in illegitimate profit and fined ¥86 mln.

- If the IPO were to officially collapse, AXTI would owe more than $49 mln to Chinese investors. AXTI cannot handle this, as the company has only $40 mln in unrestricted cash and short-term investments. AXTI also had $53 mln in short-term debt at end 2023 and limited operating cash flows for the last three calendar years.

- These reporting gaps are unsurprising, given that AXTI’s CFO and audit chair, Gary Fischer, was previously banned for 5 years from acting as an officer of a listed company. While Gary Fischer was a board member of Integrated Silicon Solution, he was charged by the SEC for options fraud for backdating. He settled with the SEC and repaid over $500,000 in profits and penalties. Fischer was previously CFO of ESS, where two credible activist investors alleged undisclosed related-party transactions.

- A Chinese export ban that took effect in December 2023 could affect half of AXTI sales.

- The company has had plenty of troubles in its 20-year past: in 2004, AXTI settled a lawsuit that alleged “material misrepresentation concerning AXT’s operations and performance.”

- AXTI’s business is in commodities. It is low-margin and cyclical. The company competes with large conglomerates like Sumitomo and is susceptible to even the slightest competition. We even see in AXTI’s filings that a former employee copied AXTI’s process and started his own company to compete.

FEATURED REPORTS

|

November 27, 2023

MVSTStill a China Hustle

|

|

January 24, 2023

ISPRInsider Enrichment Scheme,

|

May 28, 2020

NGPipe DreamFor the last 15 years, we believe NovaGold’s management team has systematically misled investors with subjective presentation of information about a deposit so remote and technically challenging that the mine will never be built. During that time, management has been treating this 12-person concept company like an ATM, awarding themselves base salaries that rival those of the CEOs at Newmont and Barrick and total compensation packages comparable with those at Rio and BHP. If the information from the company’s feasibility studies were presented in a more honest light, investors would understand that the Donlin deposit, of which they own 50%, is not feasible to put into production at any gold price.

We think management misleads investors with custom metrics designed to deceive, directing investors to presentations which claim the deposit will require $6.7 bln in capital, however, the feasibility study clearly shows this number is $8 bln (already, we believe, far too low). The proposed natural gas pipeline central to powering the project is dead on arrival. The terrain around the Donlin deposit is among the most inhospitable on the planet. Based on recent cost-per-inch/mile data we obtained from ICF, we show the costs of the pipeline (if someone were even to attempt to build it) are likely in excess of $3 bln, two to four times higher than management’s previous forecast. One engineer we spoke with who worked on costing the pipeline told us he doesn’t know of any engineering company that has the experience to build such a complex pipeline. Management has a long history of over-promising. The Galore Creek project, once promoted as the company’s key asset, was quietly sold at a loss in 2018 after revised capex estimates increased by 5x. In short, this is a stock promote, not a mining plan. |

October 7, 2021

FFIEMove Over, Lordstown:

|

Cartoon by Johannes Leak

Disclaimer

The reports and other commentary displayed are for information purposes only and should not be relied upon as investment advice. The information provided is not a complete analysis of every material fact regarding any country, region, or market. Because market and economic conditions are subject to change, comments, opinions and analyses are rendered as of the date of this posting and may change without notice.

Opinions are intended to provide insight on macroeconomic issues and commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy.

Investments involve risk. The value of investments can go down as well as up, and investors may not get back the full amount invested. The information contained in these reports has not been reviewed in the light of your personal financial circumstances. Reliance upon the information is at your sole discretion.

The reports and other commentary displayed are for information purposes only and should not be relied upon as investment advice. The information provided is not a complete analysis of every material fact regarding any country, region, or market. Because market and economic conditions are subject to change, comments, opinions and analyses are rendered as of the date of this posting and may change without notice.

Opinions are intended to provide insight on macroeconomic issues and commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy.

Investments involve risk. The value of investments can go down as well as up, and investors may not get back the full amount invested. The information contained in these reports has not been reviewed in the light of your personal financial circumstances. Reliance upon the information is at your sole discretion.