Be warned. We are activists, usually on the short side. We are biased.

We do our best to find and present facts, based on extensive primary research and using public sources.

But we will profit if these stocks decline or, when we are long, rise in value.

We do not offer advice on how to trade a stock. We present our views.

We do our best to find and present facts, based on extensive primary research and using public sources.

But we will profit if these stocks decline or, when we are long, rise in value.

We do not offer advice on how to trade a stock. We present our views.

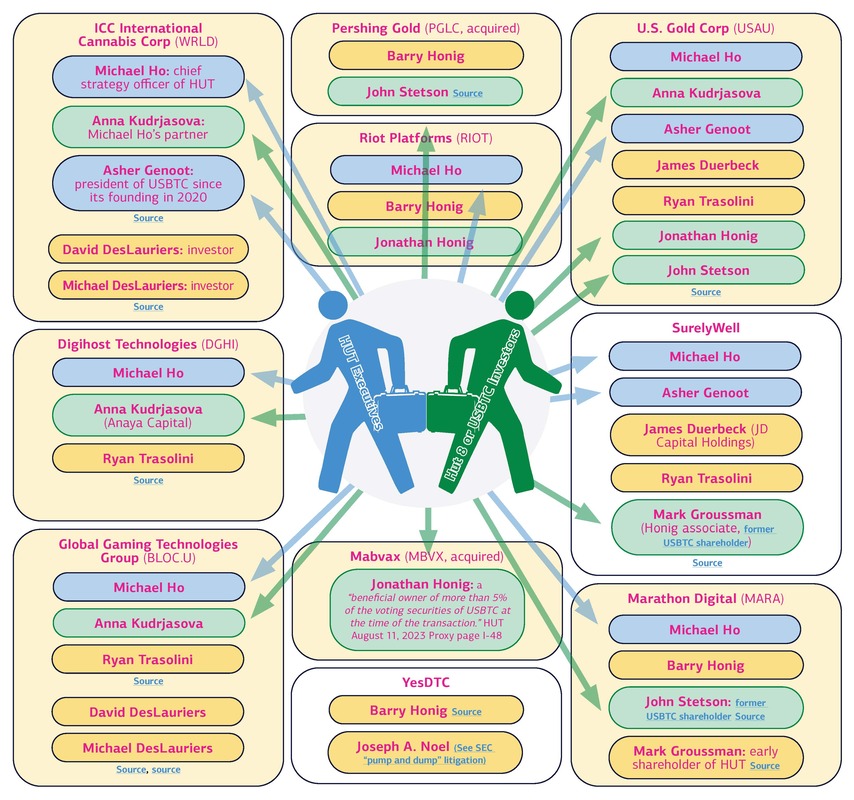

J Capital is short biote Corp. (NASDAQ: BTMD) |

|

BTMD May Make You Sick

Dangerous Side Effects, Unapproved Facilities,

Ties to a ‘Snake Oil’ Salesman, Share Dilution Coming

- BTMD offers hormone and “nutraceuticals” products that purport to slow aging and increase sex drive. But many former patients say the treatments make people sick, sometimes fatally.

- Patients often get irritable, develop acne, experience voice changes, and grow facial hair. Dangerous side effects can include cancer and cardiac problems. One lawsuit says that the (male) patient “developed breast cancer specifically as a result of the “improper, inappropriate, unsafe, and unnecessary hormone therapy that he received . . .per BioTE’s hormone replacement Pellet Therapy program.”

- An FDA inspection of BTMD discovered over 4,202 adverse events related to BTMD products that had not been reported.

- BTMD does not test products coming out of the compounding facilities and sometimes ignores appropriate hormone release levels. A 2021 lawsuit alleges that BTMD instructed its “trusted providers” to “patently disregard the patient’s objective Testosterone lab values.

- One of BTMD’s three suppliers has been accused of blinding patients due to negligence.

- We believe BTMD’s business could be cut by over 70% if the FDA determines that the hormone treatments it pushes need to be regulated as drugs.

- A key supplier has “received approximately 26 reports of adverse events related to your Testosterone and Estradiol implantable pellets, including reports of death, heart attack. stroke, When we asked clinicians, they were unaware of the adverse events.

- To promote its products, BTMD reports “studies” that say “hormones are compounded in . . . licensed FDA outsourcing centers and are held to strict standards.” But BTMD’s suppliers have been told by the FDA that their facilities do not meet the standards for a licensed compounding facility.

- BTMD’s CEO was head of the Amen Clinics, called a “scam” in Reddit posts, which describe founder Daniel Amen as a “snake oil salesman” and “scam artist.” Amen partners with BTMD. The Amen Clinics purport to diagnose ADHD, Alzheimers, and many other conditions via brain scans. They don’t.

- The CEO has little experience in consumer healthcare - except for her recent stint at Amen. In 2017, she was formally accused of fraud via “unjust enrichment” through a related party.

- A clinician told us that customer retention is tough for BTMD, because they often get doses wrong, and many clinics prefer to figure out dosing and delivery methods themselves. Another clinician told us BTMD has a problem with poorly formulated pellets popping out, especially from male patients.

- BTMD has changed CFOs twice since 2022. Those CFOs left under a cloud.

- We are puzzled that BTMD can attract any investors with growth of 4% YoY in Q1 2024, barely keeping up with inflation, a 43% decline YoY in operating cash flow, and a price of about 100x earnings.

- A wall of shares is coming to the market, indicating massive dilution for shareholders.

- BTMD had to agree to purchase from its own founder almost $77 mln in stock to settle a lawsuit in which the founder called BTMD’s SPAC merger a “get rich quick scheme.”

- The company’s disclosure of legal proceedings fills two pages of the 10K.

FEATURED REPORTS

|

November 27, 2023

MVSTStill a China Hustle

|

|

January 24, 2023

ISPRInsider Enrichment Scheme,

|

June 27, 2023

LIBehind the Latest Lithium

|

October 7, 2021

FFIEMove Over, Lordstown:

|

Cartoon by Johannes Leak

Disclaimer

The reports and other commentary displayed are for information purposes only and should not be relied upon as investment advice. The information provided is not a complete analysis of every material fact regarding any country, region, or market. Because market and economic conditions are subject to change, comments, opinions and analyses are rendered as of the date of this posting and may change without notice.

Opinions are intended to provide insight on macroeconomic issues and commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy.

Investments involve risk. The value of investments can go down as well as up, and investors may not get back the full amount invested. The information contained in these reports has not been reviewed in the light of your personal financial circumstances. Reliance upon the information is at your sole discretion.

The reports and other commentary displayed are for information purposes only and should not be relied upon as investment advice. The information provided is not a complete analysis of every material fact regarding any country, region, or market. Because market and economic conditions are subject to change, comments, opinions and analyses are rendered as of the date of this posting and may change without notice.

Opinions are intended to provide insight on macroeconomic issues and commentary is not intended as individual investment advice or a recommendation or solicitation to buy, sell or hold any security or to adopt any investment strategy.

Investments involve risk. The value of investments can go down as well as up, and investors may not get back the full amount invested. The information contained in these reports has not been reviewed in the light of your personal financial circumstances. Reliance upon the information is at your sole discretion.